12 Dec 10 Steps To Prepare Your Finances For Retirement

After years of saving during your working years, what changes should you make to prepare your finances for retirement?

When your paycheck stops, you’ll depend on your portfolio to fund your living expenses.

It’s a scary shift in the way you use your money.

Moving from the “Accumulation Phase” to the “Decumulation Phase” is a strategic shift in your goals and requires planning as you prepare for retirement.

In the words of a recent email from a reader, it’s enough to make your head spin.

With her permission, I’m sharing Rachel’s email and providing these “10 Steps to Prepare Your Finances For Retirement” as a response.

If you’re planning for retirement, today’s post is for you.

If you’re preparing for retirement, here are 10 steps you need to take to position your finances. Share on X

Moving from the “Accumulation Phase” to the “Decumulation Phase” is likely the biggest financial change you’ll go through in life. It raises some questions:

- How should I modify my portfolio in preparation for retirement?

- What changes need to be made to build a “Retirement Paycheck?”

- How do you go about the process without being overwhelmed?

- How do you know you’re really ready to retire?

The significance of the change can cause anxiety, as illustrated by the following email I received from Rachel (emphasis added by me), which was the trigger for writing today’s post.

Hi Fritz!

I’m a long-time reader and fan of yours and we are coming up on our retirement very soon. Just an idea for a blog post…

In all the planning, my head is spinning, as I try to allocate the appropriate investments into the “right” cash flow buckets (bucket strategy), while at the same time optimizing tax structure for all those investments, while at the same time accounting for social security amounts and taxes, while at the same time figuring out the best plan for Roth conversions. It all becomes a bit overwhelming and has me wondering just how important this level of detail really will be! There must be a more streamlined way of making all of these calculations to optimize all of my accounts and amounts!

Specifically, I would love to see a blog post where you talk about how you managed to reconcile all of these strategies in unison (without losing your marbles in the process lol).

Best regards,

Rachel

10 Steps To Prepare Your Finances For Retirement

Below are the 10 steps I suggest to Rachel and anyone approaching retirement as you prepare your finances for retirement. It’s an exhaustive list and will require some time to implement. Start early (1-2 years before retirement), and work through the steps methodically. Ideally, they’d be taken in the sequence presented.

1. Start Building Cash

In our working years, most of us were comfortable carrying a 1 – 6 month “Emergency Fund” of cash. In retirement, however, most folks should have a larger cash cushion (1 – 3 years is recommended) to mitigate the Sequence of Return Risk and reduce the need to sell stocks after a downturn. Increasing your cash reserves by 2+ years of spending is a big task and will take some time to implement.

In my final 18 months of work, I reduced contributions to my 401k plan (keeping only the 6% matched) and increased our after-tax contributions to a Money Market Fund. We also directed 100% of my bonus in my last two years to the MMF.

In Step #5, we’ll evaluate your risk tolerance to help you fine-tune how much cash you should carry. For now, I’m listing “Start Building Cash” as your first priority since it takes a while and will be necessary for all but those with the highest risk tolerance.

2. Estimate Your Retirement Spending

Ultimately, retirement is a math equation.

- If Spending

- If Spending > Income, you can’t.

It sounds easy, but how do you put numbers into that formula? (Therein lies the rub.)

As you prepare your finances for retirement, estimating your retirement spending is a critical part of the process that is sometimes overlooked. How will you know how much cash to build if you don’t know how much you’ll need each year? As I outlined in the first post of my When Can I Retire Series, we tracked every dime we spent for 11 months before I retired. Having established a firm baseline, we then estimated how things would change once we retired. The big ones:

- Since I retired at age 55, we’d have to pay for private insurance for 10 years.

- With our relocation to the mountains, the downsizing move eliminated our mortgage.

- With our dreams to travel, we had to build in an estimate for the RV, truck, and camping expenses.

- Knowing we wanted to do Roth conversions, we had to estimate the related tax expenses.

Focusing on your spending estimate early in the process is helpful since, by definition, it also requires you to think about critical retirement spending issues (health insurance, travel, taxes) that could otherwise be overlooked.

Yes, it’s a painful process.

But it’s critical.

3. Determine Your Retirement Income

With the first part of the formula in place, it’s time to turn your attention to the second. How much income can you safely produce in retirement? I addressed this in detail in the second post of the When Can I Retire Series, summarized below.

There are two main elements to consider:

- Known Income (Pension, Social Security)

- Variable Income (Portfolio Withdrawals, part-time work)

I’d suggest you focus on the Known Income first, it’s easier. Learn about Social Security Claiming Strategies to determine when to start receiving those benefits (you don’t need to finalize your decision at this point, but it’s helpful to have an idea). If you choose to delay (like me), you need to determine the portfolio withdrawals you’ll need to bridge those extra years. If you are lucky enough to have earned a pension, get updated pension estimates for various retirement dates and determine your start date for the pension.

To estimate your Variable Income, update your Net Worth Statement and subtract any assets that won’t be used to fund retirement (See line 56 in this spreadsheet for my formula, which subtracts cars, home equity, etc). The result is your “Retirement Assets” which can be used to fund retirement. If you’re still a few years out from retirement, add a few columns to calculate your projected Net Worth by future year, and copy the Retirement Asset formula to see the impact of waiting one year, two years, etc.

Once you know your Retirement Asset figure, multiply it by 3%, 3.5%, and 4% (lines 59-60) to determine a “Safe Withdrawal Rate” you can safely spend from your assets.

Finally, add in any part-time income you expect to earn in retirement. Be conservative, you don’t want to be dependent on an optimistic income and find yourself falling short once you’ve retired. As I’ll outline in Step #5, it’s best to hedge your bets and be surprised by the good vs. being too aggressive and finding yourself short after you’ve retired.

Add the Known and Variable Incomes together, and compare them to your estimated spending.

Voila. Math problem solved.

You now know if you’re ready to retire from a financial perspective. Don’t forget to spend some time thinking about the non-financial aspects of retirement. That’s beyond the scope of today’s post, but is something I write about frequently (see “7 Secrets To A Great Retirement” for an example).

It’s important, don’t overlook it.

4. Quantify “The Gap”

“The Gap” is an important concept as you plan for retirement.

Once you’ve determined your income sources in Step 3, determine “The Gap” by subtracting your Known Income (Pension, SS) from your Retirement Expenses. For example, if your estimated spending is $80k and you’ll have $30k from SS, your “Gap” would be $50k ($80 – $30 = $50).

It’s also important to realize that “The Gap” could change from year to year, especially if you’re planning on delaying your Social Security. Using the above example (and eliminating inflation for simplicity), let’s assume you’re retiring at age 63 and won’t claim SS until age 70. The gap would be $80k for those first 7 years, then drop to $50k at age 70.

In addition, perhaps you’re planning on doing Roth conversions before taking Social Security (assuming it won’t disqualify you from ACA Health Insurance subsidies.) If the $80k covers “normal” spending, recognize there will be an additional tax expense for those Roth conversions, creating a larger gap in your early retirement years.

Another “Gap” that some folks don’t consider is when you can access your retirement funds. If you’re retiring before the age of 59 1/2, make sure you include an analysis of how much money you have in your accessible after-tax accounts to “bridge the gap” until you can access your retirement funds (another reason Step #1 is so important, especially if you’re retiring early). There are some techniques to access retirement money before age 59 1/2 (such as the Rule of 55), but they’re outside the scope of this article.

The Gap, and how it changes with time, impacts how you prepare your finances for retirement.

To help visualize how things change with time, we built a simplified retirement cash flow spreadsheet that modeled our income and spending from retirement at age 55 through age 95. You can look at it here, but I would suggest you build your own (I took a shortcut with my tax calculation that I don’t like in hindsight).

A better solution would be to use Bolden Financial Planner, a robust and helpful tool to visualize your retirement cash flow over your lifetime. I’m a proponent of the Bolden software and recommend it to anyone in the planning stages of retirement. Since you’ve already updated your Net Worth and estimated your spending and income, you’re ready to plug those numbers into Bolden. I used it in addition to my spreadsheets when planning for my retirement, and recommend it to all of my readers.

It’s important to understand your Gap and how it changes over time. We’ll use this knowledge in Step 7.

5. Hedge Your Bets

Once you’ve reached this point, it’s time to step back.

Where are you being too optimistic? What have you missed? Can you get health insurance for the price you estimated, or should you add a hedge? Can you get by with that 4% SWR, or will a higher (and more risky) withdrawal rate be required?

It’s time to ask yourself about risk. How much are you comfortable with? How will you react if there’s a bear market the month after you retire? Take this free (and quick) Risk Tolerance Assessment to see where you rate on this scale:

Consider adding some hedges into your calculations if you have an average or lower risk tolerance. We estimated most of our expenses on the higher end, and it’s been enjoyable in retirement to see our actual spending come in lower than forecast.

Knowing your risk tolerance also helps you establish the size of your cash reserve and asset allocation, which we’ll discuss in Steps #7 and #8 below.

6. Analyze Your Current Reality

This is where the fun starts.

Before you can determine how to prepare your finances for retirement, you must have a clear view of your current situation. I wrote Our Retirement Drawdown Strategy a year before I retired, and encourage you to begin writing your strategy at this stage in the process (use my article as an example).

Below are two charts from the first page of our strategy, which show how I thought through the “Analyze Your Current Reality” step:

Once we had a clear view of our current reality, we identified the steps we needed to take to prepare our finances for retirement. You’ll figure this out as you work through the remaining steps, and I encourage you to add them to your strategy as you decide what changes are appropriate for you. In our case, the main steps included:

- Delay The Pension

- Do Roth Conversions

- Implement The Bucket Strategy

- Improve our Tax Location Efficiency

- Figure out Health Care Insurance

- Delay Social Security

- Several Other Items I put under “Longer Term”

Again, the Bolden Financial Planner is a great tool to capture your current state and evaluate the impact of various approaches in your Withdrawal Strategy. If you do nothing else with today’s post, I hope you evaluate that tool – it’s the best one that I’m aware of for those who are trying to figure out how to prepare your finances for retirement.

Note: If you’re curious about how our Drawdown Strategy played out, you can read the update I wrote titled “Revising Our Drawdown Strategy After 3 Years of Retirement.”, where I gave ourselves a grade for every major element in the strategy (3 A’s, a B and a B-). I’m also considering a third article in the series, looking at our Drawdown Strategy after 6 years of retirement, using the 12/31/24 data for the update. Stay tuned for this one early in 2025…

7. Design A Retirement Paycheck

One of the biggest steps as you prepare your finances for retirement is to decide what system to use to replace your paycheck. In essence, how will you fund “The Gap?”

We decided to use The Bucket Strategy, which I’ve written about extensively in The Bucket Strategy Series. The main thing I like about this strategy is the mental model represented by the 3 buckets and the peace of mind Buckets 1 and 2 provide against stock market volatility. We’re sleeping well at night, and that’s worth a lot. Here’s a summary of the three buckets:

- Bucket 1 / Cash: Short-term retirement spending (2-3 years of spending)

- Bucket 2 / Bonds: Mid-term spending, hedge against bear markets (4-6 years of spending)

- Bucket 3 / Stocks: Long-term spending, inflation protection (remainder of the portfolio)

In summary (read the series for the details), The Bucket Strategy provides a monthly transfer from our CapitalOne Money Market Fund into our checking account. Once it’s set up, there’s no need for budgeting and no anxiety about spending if we have the money in our checking account.

To use our example from Step #4 above, if your “Gap” is $50k, you’d hold $100k – $150k in cash and transfer $4,166/month ($50k/12 months) into your checking account each month. As Bucket 1 declines over the year, you’d refill it from either Bucket 2 or Bucket 3, depending on which asset class has outperformed (we use our Asset Allocation to determine our refill strategy, as I discuss here).

As your “Gap” evolves, you can resize Bucket 1 accordingly. Once Social Security starts, for example, you can reduce the amount of money held in Bucket 1 since “The Gap” will now be smaller than it was before receiving Social Security. If you get some part-time income, you can use that to refill Bucket 1. You may also want to convert your dividends to cash (vs. automatically reinvesting) in your after-tax accounts, a move we’ve made to ease the refilling process.

We’re 6 years into retirement, and those monthly paychecks continue to flow. It’s worked well for us, but it’s far from the only way of replacing your paycheck. (Watch this video from Rob Berger for an argument in favor of simply using a 60/40 portfolio).

The key elements to consider are to build an approach that provides:

- A system to automatically transfer funds into your checking account.

- A mechanism to cover “emergency expenses” without exceeding your SWR. (see Q5 in this article)

- A cushion of cash and bonds to minimize your risk of selling stocks in a Bear Market.

- A system to rebalance between Asset Allocation classes at least once/year.

The important thing is to decide and then set up a system that works for you BEFORE you retire. Regardless of the path chosen, it is critical to establish a cash buffer before your paycheck stops. Imagine a Bear Market crash immediately after you retire, and you’ll quickly realize the importance of having your protection in place before your retirement date. (There’s a reason I listed “Start Building Cash” as the #1 Step.) Selling stocks in a downturn is one of your biggest risks in retirement, and you must have a system in place to avoid that before your retirement begins.

8. Modify Your Asset Allocation To Align With New Risks

As you prepare your finances for retirement your asset allocation will likely need to be modified as you approach retirement.

Why?

Your Asset Allocation should be aligned with your risk tolerance, and your risk tolerance will change dramatically in retirement. As one example, your “Human Capital” and ongoing paycheck were your buffers against a Bear Market while you were working, reducing your risk. Those will be gone (or greatly reduced) in retirement, and you’ll be far more exposed when the next bear market arrives (and there WILL be a bear market, or two, or three during your retirement). In addition, you’re now depending on your portfolio to cover your expenses, which adds additional risk.

We’ve already discussed increasing your cash buffer in Steps 1 and 7, but it’s worth looking at your Stock/Bond mix to see if you’re too exposed to stock market volatility.

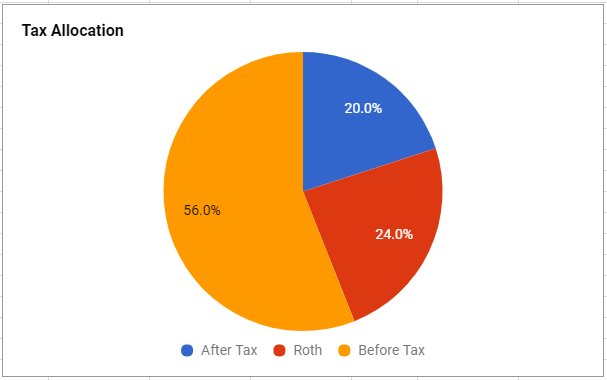

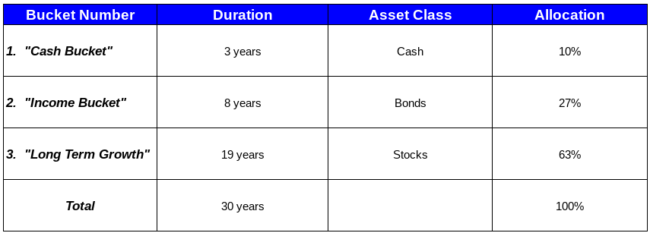

The Bucket Strategy automatically defines your initial asset allocation for retirement. In Your Bucket Strategy Questions, Answered!, I addressed a question regarding The Bucket Strategy and Asset Allocation which is relevant. Assuming you’ve saved 30 years’ worth of spending in your portfolio, Bucket 1 (Cash) will become 10% of your portfolio (3 years / 30 years). Your decision on how many years you’re going to hold in each bucket automatically leads to an asset allocation, as presented in the example below from that article:

You may consider adding a Bond Ladder into your strategy, which we’ve done recently. I explain the details in How To Build A Bond Ladder and feel it is a better structure for years 2-5 versus going with a Bond mutual fund or ETF, which can experience fluctuations in value based on interest rate changes. With a bond ladder, you’ll be holding the bonds to maturity, locking in the rate of return and allowing you to better predict your future income.

If you decide to use a system other than The Bucket Strategy to develop your retirement paycheck, take some time to review your current asset allocation and consider “de-risking” it before retirement. A standard “rule of thumb” (I hate those) is on the order of 60/40 stocks to bonds, but your risk profile from Step 5 should be considered as you finalize your asset allocation.

One final point, especially for those without a pension. As you’re working on your Asset Allocation, it’s reasonable to evaluate Annuities as part of your plan. The annuity payment will, in effect, reduce the “Gap” that you’re covering with your portfolio. Use Immediate Annuities to get some current estimates. For example, a 60-year-old man could get a $586/month payment for life in return for a $100k investment (a 7% annual payout rate, which justifies consideration). Annuities are typically best suited for lower-risk individuals without a base income (pension), though they could also be used as a shorter-term bridge to Social Security. (For example, if you’re retiring at 65 and want to delay SS until age 70, a 5-year certain annuity would pay $1,844/month for the same $100k investment, but would only pay from age 65 to age 70).

9. Consider Roth Conversions

An important consideration as you prepare your finances for retirement is whether to pursue Roth Conversions in your early retirement years before the dreaded Required Minimum Distributions kick in. I’ve discussed Roth Conversions in detail in The Golden Years of Roth Conversions, and would encourage you to read that article for more background.

From a planning perspective, the decision on whether to pursue Roth has a major impact in the following areas:

- Impact on ACA health insurance subsidies (if you’re retiring before age 65).

- Increased spending requirements to cover the additional tax expense.

- Potentially closing your 401k to make Roth conversions easier.

- IRMAA Surcharges on Medicare premiums (if you’re doing Roth conversions at age 63 or later).

Recognize your Quarterly Estimated Tax payments will be higher when doing Roth conversions, and ensure you’ve planned sufficient income to cover the additional expense. We also found it difficult to process Roth conversions from our 401k, so we said Goodbye To Our 401k and rolled it over into our individual IRA account to simplify the process.

As I was writing this article, I read Optimizing ACA Subsidies vs. Roth Conversions, an excellent article weighing the pros and cons of doing Roth conversions while also maximizing ACA subsidies. It’s worth a read if this applies to you.

Finally, the Bolden Financial Planner is an excellent tool for evaluating whether Roth conversions make sense. It provides an assessment of your lifetime tax expenses under various scenarios and helps make your decision. If you’re planning for retirement and haven’t yet explored this product, I strongly recommend it.

10. Implement A Year-End Financial Review

If you’re not already doing an annual financial review, it will be critical to start one in retirement. In my article “A Step-By-Step Guide For Your Annual Financial Review” I provide a detailed checklist of things you should cover in your annual review, including items specific to post-retirement years.

At a minimum, you must have a method to update your net worth, monitor your annual spending, rebalance your asset allocation, refill your buckets, and determine your Safe Withdrawal Rate for the following year.

Conclusion: How To Eat The Elephant

For my conclusion, I’ve decided to share my e-mail response to Rachel, which I wrote on November 25th. I wrote the e-mail in a few minutes, whereas I’ve spent hours writing today’s post. I’m pleased to see this article was consistent with my original response, and consider it an appropriate (and Pithy) summary of everything I’ve written above.

Rachel,

Thanks for taking the time to send your note (and for reading my blog!). The most important 5 words in your email are “while at the same time.”

There’s no need to do it all at once. Like eating an elephant, the important thing is to figure out which bites to take, and in which order. Eating the entire elephant in one sitting will, indeed, cause you to lose your marbles. So, develop a strategy, including a sequence of what steps you need to take, and when you need to take them. It takes a while to eat the elephant, so be patient.

You’ll then need to get a good estimate on your annual spending in retirement, and your known income flows. The difference between the two is the amount you’ll need to pull from your investments, and you’ll need to calculate your Safe Withdrawal Rate to ensure you have sufficient savings to cover your retirement spending needs. As part of this process, you’ll have to determine if you’d like to do Roth conversions in your early retirement years, and how much cash you’ll need to cover the taxes incurred as a result.

I hope that helps in the short term.

Longer term, I think your idea of writing a post on the topic is a good one…

Your Turn: What steps are you taking to prepare your finances for retirement? Were any of these 10 items a surprise? If you’ve already retired, what advice would you give those approaching retirement? Let’s chat…